New Launch vs Resale Condo: The Strategic Choice Every Buyer Faces

The Singapore property market has always been a paradox of logic and emotion.

Buyers want “value,” yet chase “new.” They talk about rental yield, yet crave capital gains.

And at the heart of this tension lies one deceptively simple question:

Should I buy a new launch or a resale condo?

In 2025, this question is harder than ever to answer — because both choices are shaped by a new macro environment:

- Higher interest rates (3.8–4.2%)

- Tight ABSD and TDSR policies

- A record number of TOPs between 2025–2027

- Rising construction and land costs

- Flattening income growth

So the “better” choice isn’t about amenities or layout.

It’s about how you time the property cycle, manage liquidity, and hedge your risk exposure.

Let’s unpack this with data, clear logic, and behavioral insight—guided by Singapore’s Property Launcher.

Understanding the Core Difference

Before diving into numbers, let’s strip both choices to their economic essence.

| New Launch Condo | Resale Condo | |

| Economic nature | A forward contract on future housing supply | A spot purchase of a current asset |

| Payment flow | Progressive, deferred | Immediate, full disbursement |

| Primary risk | Construction, timing, market volatility | Condition, lease decay, liquidity |

| Psychology | Hope, projection, speculation | Certainty, pragmatism, yield focus |

In finance terms, a new launch is an option on future value, while a resale condo is a bond with steady returns.

Both have roles in a portfolio — but their risks and payoffs occur on different timelines.

📈 Macro Landscape 2025: Why the Game Has Changed

In the last decade, Singapore’s property narrative revolved around cheap money and rapid urban renewal.

That world is gone.

1. Interest Rates Reshape Affordability

From 2019 to 2023, mortgage rates quadrupled.

For a S$1.5M loan, the difference between 1.5% and 4% rates adds ~S$20k in annual interest cost.

This alters the psychology of leverage:

- Resale buyers feel the pinch immediately (full loan disbursement).

- New launch buyers get delayed exposure (progressive payment), but by TOP, rates may stay high — neutralizing the benefit.

Hence, financing advantage ≠ long-term cost efficiency.

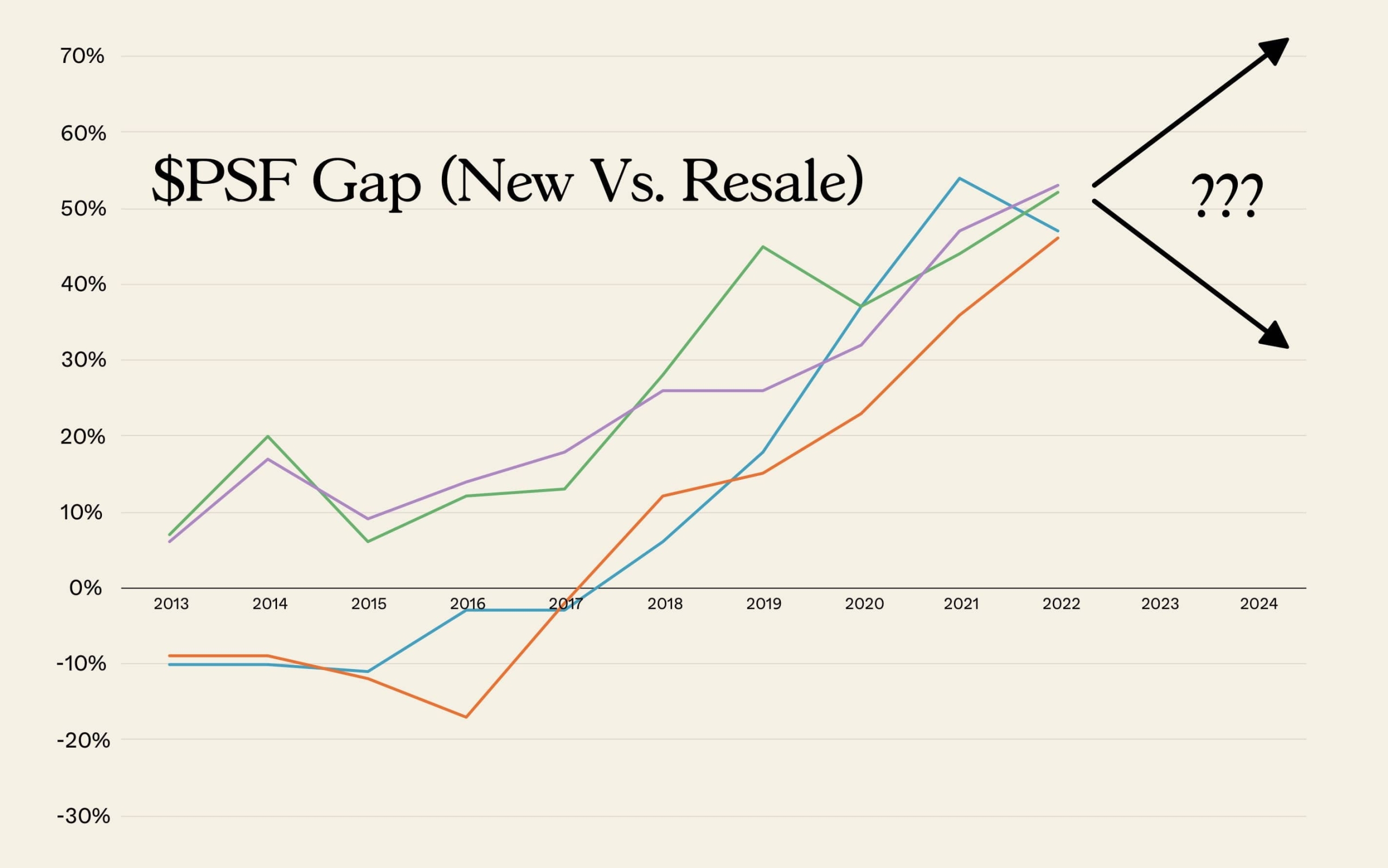

2. Price Gap Between New and Resale Has Hit a Ceiling

According to URA data, average new launch prices are 25–35% higher than nearby resale condos.

In some RCR districts, that gap is almost 40% — pricing in 5 years of future appreciation before completion.

That means buying a new launch in 2025 is like paying tomorrow’s price today.

Resale buyers, conversely, are often buying 2023 prices in 2025 due to market lag.

3. Developer Margins Are Squeezed

Land bids and construction costs are at all-time highs.

Developers can’t easily slash prices without eroding margins, so they instead use marketing optics (e.g., small unit sizes, deferred payment plans).

But that means new launches are less underpriced than they used to be.

The “sure win” playbook of 2010–2020 — buy early, flip at TOP — now carries more timing risk.

4. Rental Yields Have Peaked (Short-Term)

The post-COVID rental boom plateaued by mid-2024.

High rents (up ~45% since 2020) are now meeting tenant resistance.

Yield compression is likely — favoring resale owners who already locked in earlier low prices, not new launch buyers entering at elevated valuations.

5. Demographics and Urban Policy

The government’s push for decentralization (Tengah, Woodlands, Punggol Digital District) means future value growth will spread laterally, not vertically.

New launches in untested areas may take a decade to mature; resale condos near established nodes may outperform via consistency.

Deep Dive: Down Payment & Financing Flows

The down payment for new launch vs resale condo isn’t just a number — it’s a liquidity decision.

🏗️ New Launch

- 5% booking fee (cash) + 15% upon signing.

- Loan disbursement over 3–4 years.

- Early years = low monthly payments → easier cashflow, higher optionality.

- But at TOP, your loan “explodes” into full service mode, often when rates are still high.

🏢 Resale

- 5% cash + 20% CPF or cash immediately.

- Full loan disbursed; interest starts now.

- Immediate ownership and rent offset.

- Requires stronger upfront liquidity but clearer debt horizon.

This is time-value arbitrage:

- New launch buyers are borrowing from the future.

- Resale buyers are paying for the present.

The Investment Lens: Yield, IRR, and Risk Curves

Let’s model both under realistic 5-year scenarios (2025–2030).

| Metric | New Launch | Resale Condo |

| Purchase PSF | $2,150 | $1,680 |

| Entry Price | $1.45M | $1.3M |

| Rental Income (5 yrs) | $0 (construction) + $42k/yr after TOP | $45k/yr immediately |

| Appreciation (5 yrs) | +12% | +8% |

| Maintenance/Reno | $10k | $50k |

| Loan Cost (4% avg) | $190k | $210k |

| Net Profit | ~$180k | ~$160k |

| IRR (after leverage) | ~4.9% | ~4.5% |

| Volatility (Std. Dev.) | High | Low |

At first glance, new launches win narrowly.

But IRR only tells half the story — volatility and liquidity risks tilt the scales back toward resale.

Key insight:

Resale’s lower entry price gives a margin of safety.

New launch’s progressive payment provides cashflow comfort.

Your personal time horizon decides which benefit matters more.

Behavioral Economics: Why Buyers Choose Differently

Every property purchase is part finance, part emotion.

The “new launch vs resale condo” decision exposes our cognitive biases more than any other.

1️⃣ The Novelty Bias

People assign higher value to things that feel new — even when fundamentals are equal.

Developers exploit this with showflat psychology: perfect lighting, smell of fresh paint, curated scarcity (“Only 2 units left!”).

Result: buyers overpay for emotional satisfaction.

2️⃣ The Anchoring Trap

When agents say “$2,200 psf is fair, nearby resale is $1,950,” your brain anchors on the difference, not absolute value.

But in absolute terms, that’s a $250 psf premium — or ~$300,000 extra — for something not yet built.

3️⃣ The Certainty Effect

Resale buyers, conversely, value visible certainty. They see, touch, inspect.

But they underestimate hidden maintenance or lease decay.

Their safety bias can lead to opportunity cost (missing early-stage growth).

Lesson:

Be self-aware. Your property decision is as much psychology as math.

Risk Spectrum: Which Is Truly “Safer”?

| Risk Factor | New Launch | Resale Condo |

| Construction / Delay | High | None |

| Market Timing Risk | High (TOP cycle) | Lower |

| Lease Decay | None (99 yrs) | Moderate |

| Maintenance Cost | Low early | High later |

| Liquidity / Exit | Low pre-TOP | High |

| Financing Shock Sensitivity | Moderate (delayed) | Immediate |

| Rental Stability | Unproven | Proven |

When markets are rising, new launch looks brilliant.

When markets flatten or correct, resale becomes the safe haven.

Hence, the wise investor diversifies exposure — e.g., holds both in different phases of the cycle.

Long-Term Structural Insight: The Life Cycle Advantage

Real estate cycles in Singapore roughly follow a 7–10-year rhythm:

- Land acquisition & launch (Years 1–2)

- Construction (Years 3–4)

- TOP + resale lift (Years 5–6)

- Maturity & rent stabilization (Years 7–9)

- Renewal or stagnation (Year 10+)

New launch buyers enter at Stage 1–2.

Resale buyers often enter at Stage 5–6.

So their payoff windows rarely overlap — and that’s why comparing them 1:1 can mislead.

New launch = future timing; resale = current yield.

The optimal investor rotates: buy new launch early in one cycle, switch to resale when prices overheat, collect yield, and re-enter next cycle.

That’s how institutional property funds manage risk.

For Own Stay: “Resale vs New Launch Condo for Stay” Perspective

Beyond numbers, lifestyle factors still matter.

Consider:

| Lifestyle Factor | New Launch | Resale |

| Move-in timeline | 3–5 years wait | Immediate |

| Neighborhood maturity | Developing | Established |

| Amenities | Modern, future-ready | Existing, sometimes aging |

| School proximity / transport | Often future-planned | Already operational |

| Community | To-be-formed | Stable, known |

For families with school-aged children or elderly parents, resale wins hands down.

For young professionals or couples planning ahead, new launch offers freshness and flexibility.

Advanced Analysis: Real Risk-Adjusted Returns (Sharpe-style Thinking)

Let’s express property not in simple ROI, but return per unit of risk.

| New Launch | Resale | |

| Avg. Annualized Return | 4.9% | 4.5% |

| Estimated Volatility (σ) | 8% | 5% |

| Risk-Free Rate | 2% | 2% |

| Sharpe Ratio | 0.36 | 0.5 |

Higher Sharpe = better risk-adjusted performance.

That means for each “unit” of risk you take, resale condos deliver more consistent reward.

Decision Framework (Data + Psychology)

Ask yourself these six questions:

- Liquidity horizon: Can I wait 4–5 years without seeing returns?

- Income needs: Do I need rental yield now or later?

- Debt comfort: Can I handle full mortgage immediately?

- Risk tolerance: Am I okay with paper losses during downturns?

- Location quality: Am I buying proven fundamentals or speculative storylines?

- Emotional discipline: Do I buy for ROI, or for excitement?

If you answer “yes” to 4+ of the above → go new launch.

If not → resale will serve you better.

FFinal Verdict: Which Should You Choose?

In Singapore’s 2025 property landscape, the choice between a new launch and a resale condo isn’t a strict either-or. It often reflects your investment mindset, time horizon, and how you prefer returns to take shape.

Opt for a new launch if you’re long-term oriented, comfortable with short-term price movements, and confident in Singapore’s ongoing urban growth. For buyers who prioritise future potential over immediate results, buying a new launch condo is usually a strategy built on patience and conviction.

A resale condo, on the other hand, suits those who value established performance, visible rental income, and greater flexibility when planning their exit.

In essence:

New launches reward foresight and staying power.

Resale properties reward discipline and practical decision-making.

The wisest investors own both — one for growth, one for stability.

💬 FAQs

Q1: Are new launches still worth the premium?

Only if you plan beyond 8–10 years. Short-term flippers face compressed margins.

Q2: Which has better rental yield?

Resale condos typically deliver higher yield (3–5%) versus new launches (~2–3% post-TOP).

Q3: How do down payments differ?

New launch = staged; resale = full upfront. New launch favors cashflow, resale favors speed.

Q4: What if interest rates stay high?

Resale owners feel impact sooner; new launch owners feel it later but for longer.

Q5: Can older condos still appreciate?

Yes — if lease >70 years and location fundamentals remain strong (transport, amenities, land scarcity).

Discover Singapore’s latest launches in CCR, RCR, OCR and EC—complete with live price lists, PSF ranges, floor plans and daily refreshes.

Discover Singapore’s latest launches in CCR, RCR, OCR and EC—complete with live price lists, PSF ranges, floor plans and daily refreshes.{kind=link}

Join The Discussion