In Singapore’s ever-evolving property market, resale Executive Condominiums (ECs) are becoming the smart buyer’s secret.

Why? They strike the perfect balance between affordability, private ownership, and investment potential.

After serving their 5-year Minimum Occupation Period (MOP), ECs can be sold on the open market — and that’s when they officially become resale ECs. These properties bridge the gap between new EC launches (limited eligibility, long wait times) and private condos (high entry prices).

In this guide, you’ll learn everything about buying a resale EC in Singapore in 2025 — from eligibility and pricing trends to buying steps, levies, and investor insights.

What Is a Resale Executive Condo (EC)?

An Executive Condominium (EC) starts as a hybrid housing model — built by private developers but subsidized by the government to make private housing more accessible to Singaporean families.

However, once an EC reaches its 5th year (after MOP), owners are allowed to sell their units to Singaporeans and PRs — transforming it into a resale EC.

The EC Lifecycle

| Phase | Ownership Restrictions | Who Can Buy |

| 0–5 years | MOP period (owner-occupied) | Only original buyers (Singaporean families) |

| 5–10 years | Semi-privatized (Resale EC) | Singaporeans & PRs |

| 10+ years | Fully privatized | Open to foreigners & entities |

💡 Why it matters: Once an EC enters resale status, it becomes more flexible and widely marketable — without the premium pricing of new condos.

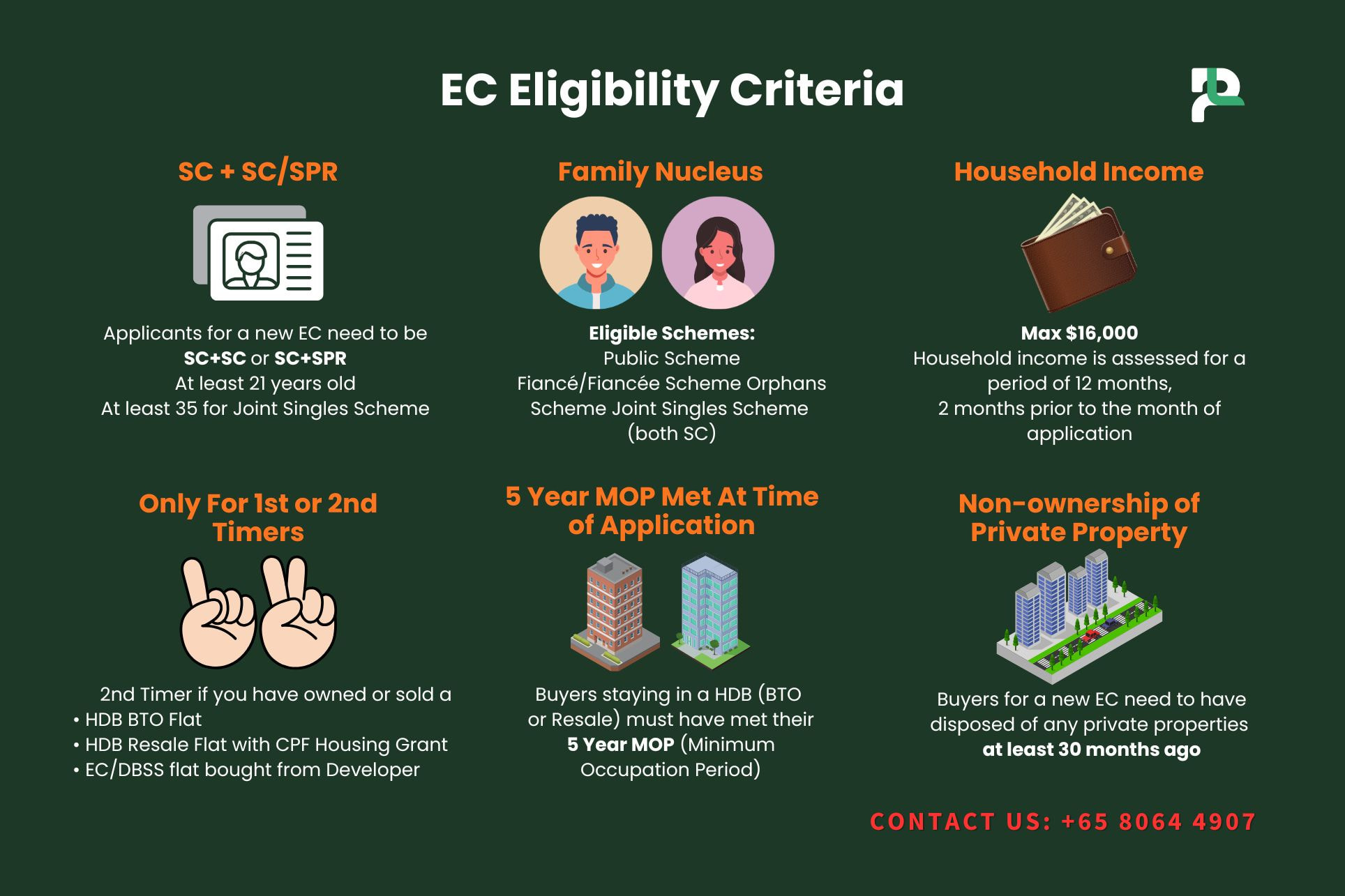

Eligibility to Buy a Executive Condo Singapore Resale

One of the biggest attractions of resale ECs is their looser eligibility rules compared to new ECs.

| Criteria | Resale EC Eligibility (After 5 years) |

| Citizenship | Singaporeans or Singapore PRs |

| Income Ceiling | No income cap |

| Family Nucleus Requirement | Not required — singles can buy |

| Ownership of Private Property | Allowed |

| Foreigners | Eligible only after 10 years (fully privatized phase) |

💬 Example: A PR couple earning $20,000/month can’t buy a new EC due to income ceiling limits — but they can buy a resale EC after MOP.

Why Buyers Love Resale ECs

| Immediate move-in | No construction waiting time. |

| Larger layouts | ECs typically offer bigger units than condos. |

| Prime locations | Often in mature estates with MRT access. |

| Lower PSF | 15–25% cheaper than nearby private condos |

No MOP restrictions for new owners.

💬 Tip: Resale ECs often come with better community amenities — pools, gyms, and BBQ decks — comparable to full private condos.

Executive Condo Resale Price Trends (2025)

ECs have outperformed expectations since 2015. As of 2025, resale EC prices have grown significantly due to strong upgrader demand and limited new EC supply.

| Project | Location | Completion Year | Avg PSF (2025) | 5-Year Change |

| The Brownstone | Canberra | 2017 | $1,330 | +60% |

| Bellewaters | Sengkang | 2017 | $1,300 | +58% |

| The Criterion | Yishun | 2018 | $1,250 | +50% |

| The Terrace | Punggol | 2018 | $1,280 | +55% |

📊 Market Data:

- Average resale EC price (2025): $1,250–$1,400 psf

- OCR private condos: $1,600–$1,750 psf

- Price gap: ~15–20% (narrowing yearly)

Understanding the Resale Levy (and Why It Doesn’t Apply Here)

The resale levy is one of the most misunderstood aspects of EC ownership.

Here’s the rule:

- It applies only when you buy a new EC from a developer after previously owning a subsidized flat.

- It does not apply when buying a resale EC on the open market.

| Previous Flat Type | Resale Levy (Family) |

| 2-room | $30,000 |

| 3-room | $50,000 |

| 4-room | $70,000 |

| 5-room | $80,000 |

✅ In short: If you’re buying a resale EC, there’s no resale levy.

Pros & Cons of Buying a Resale Executive Condo

| Advantages | Disadvantages |

| Immediate move-in | Older age (5–10 years) |

| Open to PRs & singles | No CPF grants |

| No income limit | May need renovation |

| Larger layouts | Smaller appreciation potential (post-MOP) |

| Cheaper PSF vs condos | Bank loan required (no HDB loan) |

💬 Verdict: Resale ECs are best for buyers seeking affordability, space, and flexibility — without HDB or new EC restrictions.

Resale EC vs New EC: Which Is Better for You?

| Factor | New EC | Resale EC |

| Eligibility | Singapore Citizens only (family nucleus) | Singaporeans & PRs |

| Income Ceiling | $16,000 | None |

| Grants Available | Yes (CPF Housing Grant) | No |

| Move-in Time | Wait 3–4 years | Immediate |

| Price (2025) | $1,450–$1,550 psf | $1,250–$1,400 psf |

| Capital Growth Potential | Higher (early entry) | Stable |

| Flexibility | Restricted (MOP) | Full resale freedom |

💡 Tip: If you’re an upgrader or PR who missed earlier EC launches, a resale EC gives you near-condo living — at 20% less.

How to Buy a Resale Executive Condo (Singapore)

Step 1: Check Eligibility (and Restrictions)

Who can buy:

- If the EC is 5–10 years from TOP (semi-privatised): only Singapore Citizens (SC) or Permanent Residents (PR) may buy.

- If the EC is >10 years from TOP (fully privatised): all nationalities may buy.

Key rules to verify:

| Item | Requirement / Notes |

|---|---|

| Age | ≥ 21 (≥ 18 with Court approval). |

| Financing source | Bank loan only — HDB loans not available for ECs. |

| Property count / ABSD | If you already own a residential property, plan your sell-then-buy or ABSD mitigation before offering. |

| Bankruptcy | Undischarged bankrupts require Official Assignee/creditor consent. |

| Grants / levies | No CPF housing grants and no resale levy for resale ECs. |

Do now:

- Note EC TOP year (for eligibility + lease left).

- Check remaining lease (affects loan tenure/TDSR and future resale).

- If you’re a PR buying 1st/2nd property, evaluate ABSD exposure.

Step 2: Arrange Financing (before viewing)

Target timeline: 1–3 working days for in-principle approvals.

What to secure:

- AIP (Approval-in-Principle) from 1–2 banks.

- Understand LTV and cash/CPF needs:

- If this is your first housing loan and age+tenure ≤65 years → LTV up to 75%, cash min 5%, remaining 20% cash/CPF.

- If you have an existing housing loan, LTV is lower (commonly 45%/35% bands).

- TDSR: total debt obligations ≤ 55% of gross monthly income.

- Prepare docs: NRIC, latest 3–6 months payslips/NOA, CPF contribution history, liabilities (cards/loans), IR8A/NOA for self-employed (2 years).

Costs to plan:

| Cost item | Typical amount | When / Notes |

|---|---|---|

| Bank valuation fee | ~$200–$500 | During option period when you trigger the bank valuation. |

| Legal / conveyancing | ~$2,000–$3,500 (bank-panel lawyer) | Billed through completion; confirm your bank’s panel. |

| Mortgage duty (on loan) | 0.4% of loan amount, capped at $500 | Payable when loan docs are stamped (before completion). |

| Fire insurance | ~$50–$150/yr | Required by some banks; set up before loan disbursement. |

| Mortgage term insurance (optional) | Varies by age, sum assured & tenure | Optional protection; can be arranged before/after completion. |

Pro tip: Ask the banker to model 3 scenarios: base rate, +1% shock, and partial prepayment—so you know your stress points.

Step 3: Research EC Projects (shortlist smart)

Filter quickly by:

| Factor | What to check / how to use it |

|---|---|

| Age & lease left | Newer ECs usually have higher $PSF but can offer better quantum than private condos; confirm TOP year and remaining lease (affects loan tenure/TDSR & resale). |

| Connectivity | Aim for ≤800m to MRT; note bus trunk routes and expressway access for commute and tenant demand. |

| Schools | Map within 1km/2km to target schools for P1 priority; verify exact stack distance. |

| Upcoming catalysts | Check URA Master Plan for new MRT lines, town rejuvenation, and precincts (e.g., JLD, Punggol Digital). |

| Monthly maintenance | Compare MCST fees vs facilities set; look for upcoming special levies in AGM minutes. |

| Stack specifics | Assess facing, road/track noise, afternoon sun, privacy, and lift-lobby count per core. |

| URA caveats | Review recent transacted $PSF for same project/stack type to gauge fair value and negotiation room. |

| Rentability | Check area vacancy, typical rent by bed count/stack, and expected tenant profile. |

Diligence pack to request from seller/agent:

- Latest Title/Strata area, MCST minutes (look for large upcoming works), utility bills (for sanity), inclusions list (fixtures, built-ins), renovation permits (if structural), defect history (if still within DLP for very new ECs).

Step 4: Engage a Property Agent (buyer’s rep)

How to structure it:

- Decide exclusive vs open representation. With exclusive, align KPIs (timeframe, target stacks, price band).

- Confirm who pays commission. In most resale cases the buyer’s agent co-brokes with seller’s agent so the buyer doesn’t pay, but never assume—write it down.

- Ensure your agent is comfortable with bank-valuation, CPF usage, ABSD planning, MCST due diligence, and drafting offer terms that protect you.

What your agent should do:

- Pre-screen units (noise, sun, leakage, lift-lobby).

- Pull comparables and contrarian comps (bigger/smaller stacks).

- Liaise early with banker/lawyer for OTP/exercise scheduling.

Step 5: Make an Offer (and protect yourself)

Offer mechanics:

- Typical for private/resale EC: Letter of Offer or WhatsApp/email with:

- Price, option fee, intended completion date (usually 8–12 weeks from exercise), tenancy/vacant possession, inclusion list, and conditions (e.g., subject to satisfactory bank valuation on/above price).

- If accepted, seller issues OTP (Option to Purchase) once 1% option fee is paid (cash).

- Valuation: In parallel, instruct bank for valuation to avoid low-valuation surprises. If the valuation < price, the cash top-up needed = price – valuation.

Checklist before committing:

- Confirm MCST fees and any sinking fund special levy.

- Review latest MCST AGM minutes for upcoming big ticket items.

- Check property tax band, caveat status, vacant possession date, and fixtures included.

Step 6: Exercise the OTP (14-day window typical)

Within the option period:

- Appoint a conveyancing lawyer (bank-panel if you’re taking a loan).

- Bank issues Letter of Offer; you sign the loan documents.

- Pay exercise fee (commonly bringing total to 5%—varies by deal).

- Pay Buyer’s Stamp Duty (and ABSD if any) within 14 days of OTP exercise/signing.

- Lawyer conducts title searches, caveat/encumbrance checks, and completes CPF usage arrangements.

- Fix the completion date and key handover conditions in writing.

If you need time to sell your current property:

- Consider ABSD remission pathway (tight timelines; ensure both sale & purchase lawyers and banker agree to the plan).

- Alternatively, add a long completion or rent-back clause if seller agrees.

Step 7: Finalise & Complete (8–12 weeks from exercise)

Leading up to completion:

- Lawyer exchanges requisitions with authorities, lodges caveat, and prepares completion account.

- Arrange fire insurance, final cash/CPF draw, and bank disbursement.

- Conduct a pre-completion inspection (water seepage, appliances, windows, balcony railing).

- Set up utilities and apply for season parking if needed.

Completion day:

- Lawyer meets at the seller’s lawyer’s office or bank.

- Keys + access cards released after funds are disbursed.

- You receive title documents (or bank holds if mortgaged).

Typical Buyer Cost Snapshot (for planning)

| Cost Item | When Paid | Indicative Amount |

|---|---|---|

| Option Fee | Upon OTP issuance | 1% of price (cash) |

| Exercise Fee | Within option period | Often to 5% total (deal-dependent) |

| Buyer’s Stamp Duty (BSD) | Within 14 days of exercise | Tiered % by price (plan with lawyer) |

| Additional Buyer’s Stamp Duty (ABSD) | Same as BSD | Depends on residency & property count |

| Bank Valuation | During option period | ~$200–$500 |

| Conveyancing (Buyer) | Completion | ~$2,000–$3,500 |

| Mortgage Stamp Duty | Before completion | 0.4% of loan (capped $500) |

| Caveat & Title Searches | During conveyancing | ~$150–$300 total |

| Fire Insurance | Before completion | ~$50–$150/yr |

Note: Rates and rules change—always confirm the latest LTV/TDSR, BSD/ABSD with your banker/lawyer.

Financing a Resale EC

| Item | Details |

|---|---|

| Loan type | Bank loan only (ECs are not eligible for HDB loans). |

| Loan-to-Value (LTV) | Up to 75% (subject to age/tenure and bank assessment). |

| Minimum downpayment | 25% total — at least 5% in cash, remaining 20% cash/CPF. |

| TDSR applies | Monthly debt obligations capped at 55% of gross monthly income. |

| Grants | None for resale ECs. |

| Stamp duties | See breakdown below. |

Stamp duties breakdown:

| Duty | Rate / Notes |

|---|---|

| Buyer’s Stamp Duty (BSD) | Progressive 1–6% based on purchase price/market value (whichever is higher). |

| Additional Buyer’s Stamp Duty (ABSD) | Depends on profile & property count. Examples (first property): 0% for Singapore Citizens, 5% for Permanent Residents. (Other profiles/second+ properties have different rates — confirm latest IRAS schedule before committing.) |

💬 Example: A $1.3M resale EC purchase → 25% downpayment = $325,000 (cash + CPF).

Investment Potential of Resale Executive Condos

Resale ECs have proven to be highly profitable investments — especially those located in mature towns with upcoming infrastructure.

Average Capital Gain (After 10 Years)

| Project | Launch Price (psf) | Resale Price (psf) | % Gain |

| The Tampines Trilliant | $730 | $1,300 | +78% |

| The Rainforest | $760 | $1,350 | +77% |

| The Brownstone | $810 | $1,330 | +64% |

Why Resale ECs Perform Well

- Government-subsidized entry prices → natural appreciation buffer.

- Located in suburban growth areas (OCR).

- Larger family units cater to long-term upgraders.

- Strong rental demand post-privatization.

💬 Pro Tip: Buy ECs 1–3 years after MOP — you’ll benefit from mid-term appreciation while paying below condo market prices.

Top Resale ECs to Watch in 2025

| Project | Location | Year TOP | Avg PSF (2025) | Investment Outlook |

| The Vales | Sengkang | 2017 | $1,300 | Stable demand, near Seletar Mall |

| Parc Life | Sembawang | 2018 | $1,280 | Strong upgrader interest |

| Bellewaters | Anchorvale | 2017 | $1,320 | Near LRT & schools |

| The Brownstone | Canberra | 2017 | $1,350 | MRT proximity drives demand |

Resale ECs vs Private Condos (2025 Market Comparison)

| Factor | Resale EC | Private Condo (OCR) |

| Avg PSF (2025) | $1,300 | $1,650 |

| Rental Yield | 3.5–4.0% | 2.8–3.3% |

| Buyer Pool | SG + PRs | SG + PR + Foreigners |

| Age (Typical) | 5–10 years | 0–5 years |

| Capital Growth Potential | Moderate (post-MOP) | Steady |

| Facilities | Comparable | Comparable |

💡 Insight: Resale ECs remain undervalued despite offering almost identical amenities — making them strong mid-term investments.

Frequently Asked Questions

1️⃣ Can singles buy resale Executive Condos?

Yes — singles can buy resale ECs once the 5-year MOP is completed.

2️⃣ Can PRs buy resale ECs?

Yes — PRs are eligible to buy resale ECs after the first MOP period.

3️⃣ Is there a resale levy for resale ECs?

No. Resale ECs are exempt from resale levies.

4️⃣ How do resale EC prices compare to private condos?

Typically 15–25% lower, offering higher yield and better entry value.

5️⃣ Do resale ECs qualify for CPF Housing Grants?

No — grants only apply to new ECs purchased from developers.

Conclusion

In 2025, Executive Condo Singapore Resale remain one of Singapore’s most compelling property segments — offering affordability, flexibility, and steady growth.

For Singaporeans and PRs who don’t meet new EC restrictions, resale ECs open the door to:

- Private housing at lower prices,

- Strategic locations in mature estates,

- Solid long-term capital appreciation.

💡 Key Takeaway: If you’re priced out of new ECs or condos, resale ECs provide a golden middle ground — accessible, value-rich, and investment-worthy.

“Thinking of buying a resale Executive Condo?

Compare 2025 EC prices, eligibility, and loan options — and find your perfect property today with Property Launcher.”

Discover Singapore’s latest launches in CCR, RCR, OCR and EC—complete with live price lists, PSF ranges, floor plans and daily refreshes.

Discover Singapore’s latest launches in CCR, RCR, OCR and EC—complete with live price lists, PSF ranges, floor plans and daily refreshes.{kind=link}

Join The Discussion